The Founders' Bet

Hire the hackers. Sell the policy.

Rotem Iram, the company's CEO, took the route you might expect from someone who would later try to merge security and insurance: captain in Israel's elite Unit 8200 signals intelligence corps, then McKinsey, then COO of K2 Intelligence's cyber practice, with a Harvard MBA tacked on for good measure. He co-founded At-Bay in 2016 with Roman Itskovich (data), Etai Hochman (risk), and Tilli Kalisky-Bannett.

Their bet, which sounded plausible in a pitch deck and absurd to incumbent insurance executives, was that a tiny startup could underwrite cyber risk more accurately than century-old carriers - because it would do the security work itself. Scan every applicant's external footprint. Monitor every policyholder continuously. Use that telemetry to price, advise, and intervene. Charge a premium. Pay fewer claims.

Rotem Iram

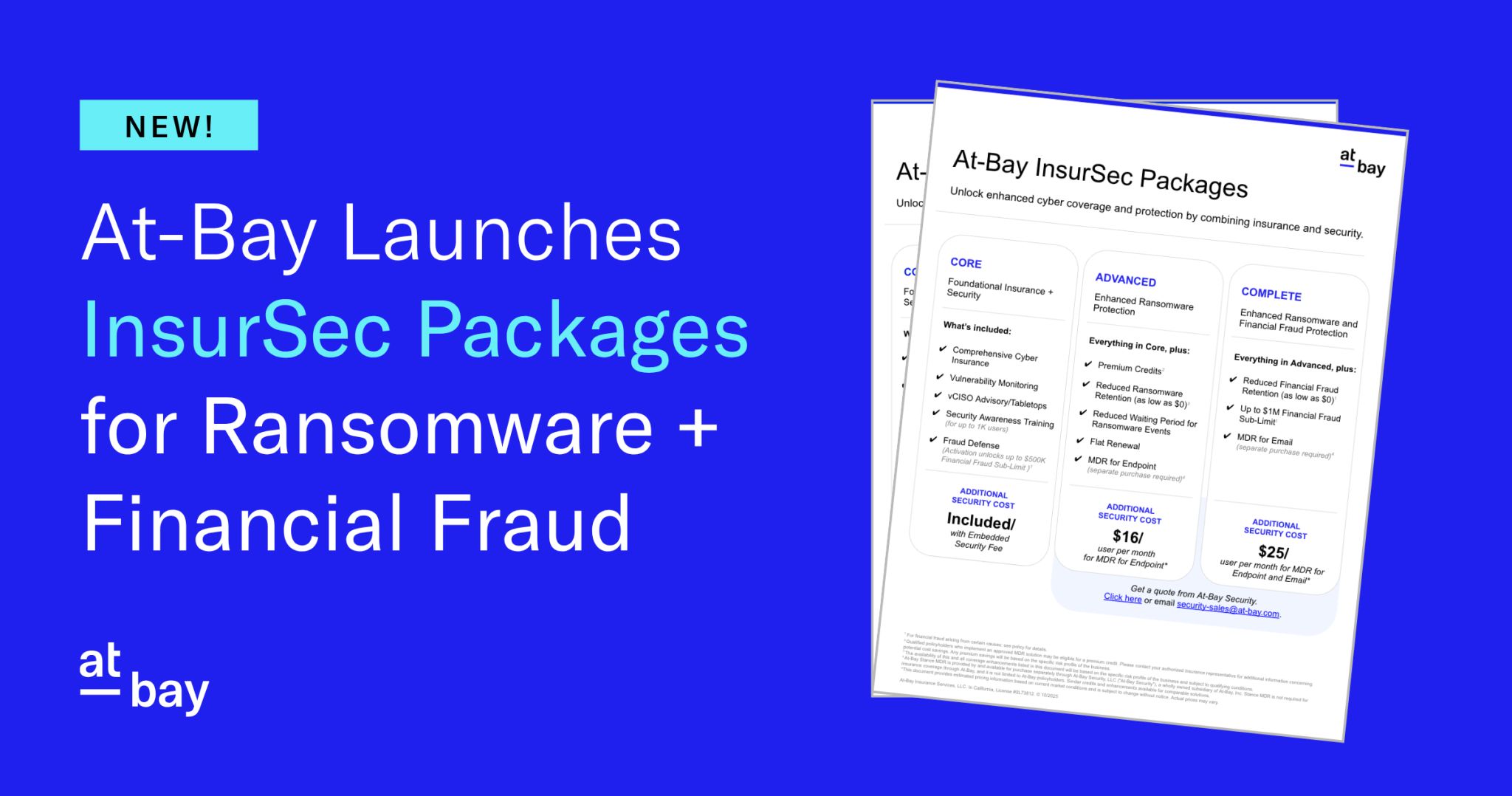

Co-founder & CEO. Unit 8200, McKinsey, K2 Intelligence. The one who calls it InsurSec without flinching.

Roman Itskovich

Co-founder & Chief Data Officer. Treats the underwriting model like a living piece of software.

Etai Hochman

Co-founder & Chief Risk Officer. Quietly responsible for the part of the business that has to be right.

Tilli Kalisky-Bannett

Co-founder. Built the early product and operations spine the rest hangs on.

Caption, with feeling. Four people, one whiteboard, a phrase nobody had marketed yet: InsurSec.