YesPress · The Profile · Filed from 560 Alabama St., San Francisco

Who they are now

The credit union, finally on time.

On a Tuesday afternoon at Listerhill Credit Union in Muscle Shoals, Alabama, a 41-year-old member opens a phone, taps three buttons, and refinances her truck. The whole thing takes nine minutes. There is no branch visit, no fax, no notary. The funding hits the dealership the same day. The credit union she joined - 90 years old, member-owned, gloriously local - has just behaved, briefly, like a fintech.

That is a Clutch transaction. There are a few thousand of them every week now, scattered across 150-plus credit unions from Suncoast to Golden 1. The software running underneath is not glamorous. It does not have a Super Bowl ad. It mostly replaces a fax machine and a clipboard. But it is, by a wide margin, the most consequential thing happening inside American community finance.

Clutch is, in the polite phrasing of its founders, a digital origination platform. In rougher English: it is the layer that lets a credit union open an account, approve a loan, fund a member and cross-sell another product without ever asking anyone to come in, sit down, and explain themselves.

When technology is as member-centric as the institutions it serves, credit unions become the obvious choice.- Clutch, from its own About page, and meant unironically

The problem they saw

America's best-loved banks have the worst software.

The financial industry has a quiet caste system. At the top sit big banks and neobanks, with their dark-mode apps and their venture money and their relentless engineers. At the bottom sit the credit unions - 4,600 of them, holding roughly $2.3 trillion in member assets, distributing the cheapest car loans in the country, and shipping product roadmaps that move at the pace of a bond ladder.

The credit unions tend to be loved. Net Promoter Scores in the 70s. People volunteer for their boards. Members refer their children. And then those children try to open a checking account online, get bounced into a 14-step form with three PDFs, and end up at Chime.

This is the problem Clutch saw, and the one it exists to solve. Not bad intent at the credit union. Just bad timing. The institutions that have been the most generous to American consumers for nine decades happen to be running on software shipped before TikTok was legal in most states.

Members didn't leave their credit union because they stopped trusting it. They left because filling out the form was harder than the loan.- Paraphrased from a Clutch sales deck, allegedly

The founders' bet

Two Stanford grads. One previous exit. A deeply unsexy market.

Nicky Hinrichsen and Chris Coleman met at Stanford's Graduate School of Business; both had also passed through MIT first. They built a used-car company called Carlypso, sold it to Carvana in 2017, and stayed on for a couple of years watching Carvana turn a 100-year-old industry inside out. The lesson they took with them was not about cars. It was about origination - the unglamorous plumbing of approving someone for a thing they want to buy.

In 2020, they started Clutch. The bet was contrarian in two directions at once. First, that the next wave of fintech would not be a new consumer brand but an upgrade to incumbent ones. Second, that the incumbents worth upgrading were not the big banks - they were the credit unions, who had distribution, trust, and absolutely no engineering bench.

This was the kind of pitch that makes generalist VCs polite. It made specialist ones write checks.

The founders, briefly

Nicky Hinrichsen · CEO and co-founder. German-born, Stanford GSB. Serves on the advisory board of Suncoast Credit Union, which is roughly the credit-union equivalent of joining your customer's family.

Chris Coleman · Co-founder. MIT undergrad, Stanford GSB. Carlypso, Carvana, and now Clutch - a man with a clear taste for industries that ought to be moving faster than they are.

The midpoint, plotted

A short company history.

2017

Carvana acquires Carlypso.

Hinrichsen and Coleman cash out of their first company. They spend the next three years asking why financial onboarding still looks like a 2008 mortgage application.

2020

Clutch is founded in San Francisco.

Initial focus: auto loan refinance for credit unions. Y Combinator joins early.

2022

Platform expands beyond auto.

Personal loans, credit cards, home equity, and deposit account opening get added. The product stops looking like a feature and starts looking like an origination stack.

2023

Series A and 100-customer milestone.

Andreessen Horowitz and TruStage Ventures back the round. Clutch crosses 100 credit union customers.

Jan 2025

$65M Series B led by Alkeon.

Total raised to $106M. a16z, TruStage and Peterson Partners follow on. The press release uses the phrase "turn credit unions into fintechs," which the headline writers happily lift verbatim.

Mar 2025

FinTech Breakthrough Award.

Named Best Loan Origination Platform. Awards mean less than revenue, but credit union procurement committees love them, so they help.

2025-2026

HAL and Emma go live.

Two AI assistants - one for lending, one for collections - move into production at multiple customers.

The product

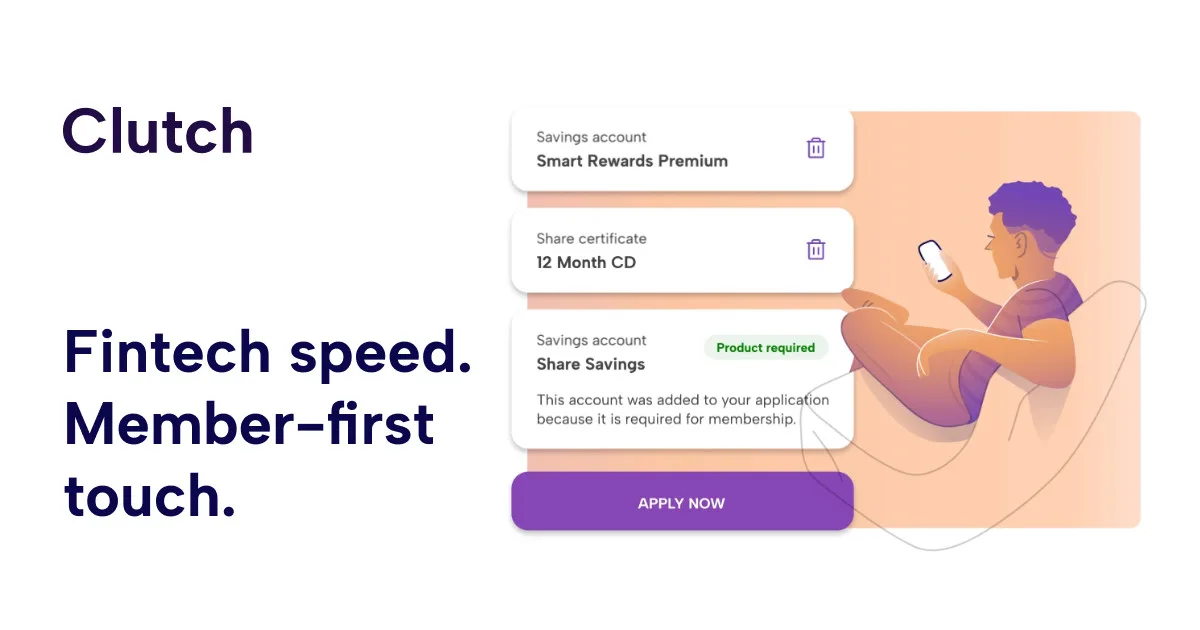

One stack, eight ways to say yes.

Clutch sells a platform, not an app. A credit union plugs it in once and gets a full set of member-facing flows, banker tools, and now AI assistants. The point is not the feature list - every fintech has a feature list. The point is what happens to the underlying numbers.

Loan Origination

Auto, personal, home equity, credit card - one application engine, branded as the credit union's.

Deposit Account Opening

Membership and deposit accounts opened entirely online, with identity verification and fraud detection baked in.

Business Account Opening

The same flow, rebuilt for the small-business members credit unions historically under-served.

Fastlane (AUS)

An automated underwriting and decision engine. Sends a yes or no without a human in the loop, where policy allows.

Targeted Remarketing

Auto loan recapture campaigns. Find members paying 11% at a captive lender and offer them 6.4%.

Data Insights

Funnel analytics built for an executive team that has never used Mixpanel and would prefer not to start.

HAL

An AI lending assistant. Helps applicants finish forms; helps lenders process them faster.

Emma

An AI collections assistant. Polite, persistent, available at 11pm on a Sunday.

We're not trying to replace the credit union. We're trying to replace the slow part.- Roughly, every Clutch demo, ever

The proof

Numbers, in the absence of marketing.

Clutch is private and does not disclose revenue. What it does disclose - and what its customer credit unions repeat in conference panels - are operating metrics that explain why the platform keeps spreading.

Clutch, in five-year strides.

Capital raised · cumulative, $M · rounded

Source: company press releases and Crunchbase. Bars are illustrative; the y-axis is not, strictly speaking, audited.

The customer roster reads like a tour of regional America: Suncoast in Florida, Golden 1 in California, San Francisco FCU in - reasonably enough - San Francisco, Listerhill in Alabama. None of these institutions are household names in Silicon Valley. All of them collectively serve more Americans than most digital-only banks do.

Credit unions handle $2.3 trillion in assets. They have been waiting, patiently, for a vendor that knows what a member is.- A paraphrase that no Clutch executive will publicly disagree with

The mission

Member-owned banking, scaled.

The thing that makes Clutch interesting, as a business, is not the technology. The technology is competent. The thing that makes Clutch interesting is the bet underneath the technology: that the right unit of distribution in American finance is not a single national brand, but 4,600 small, local, member-owned institutions that share infrastructure.

If that bet is right, then Clutch is building the missing common layer. If it is wrong, Clutch is a perfectly good loan origination vendor. Either outcome is fine, financially. Only one of them is interesting.

The unfashionable thesis

Most fintechs assume that consumers want a new brand. Clutch assumes consumers like the brand they have - they just want it to work on a phone. The first thesis has produced a lot of marketing budgets. The second one is starting to produce a lot of funded loans.

Why it matters tomorrow

A 90-year-old industry, suddenly on its phone.

Back in Muscle Shoals, the 41-year-old member who refinanced her truck in nine minutes did something the credit union has been chasing for a decade: she opened a savings account and a credit card in the next three days. Cross-sell is, in banking, what retention is in SaaS. It is the entire business model. And here it was, happening on its own, because the friction had been removed from the rest of the relationship.

That is the Clutch outcome, repeated. Not a member acquired. A member rediscovered. The credit union does what it has always done - hold the deposits, fund the loans, vote in board members - but the cycle finally turns at the speed the rest of the consumer's life runs at.

Whether Clutch becomes the AWS of community finance or just a very successful vendor is a question the next five years will answer. Either way, the Tuesday-afternoon refinance in Alabama is now a routine event. That used to take a week. That is the upgrade. That is the whole company.

Read further

Links, in approximate order of usefulness.